The second edition of the IHRSA Asia-Pacific Health Club Report was released recently in collaboration with Deloitte.

It demonstrates that the health and fitness industry in the Asia-Pacific region is in good shape – fueled by growing economies and with significant potential for continued growth.

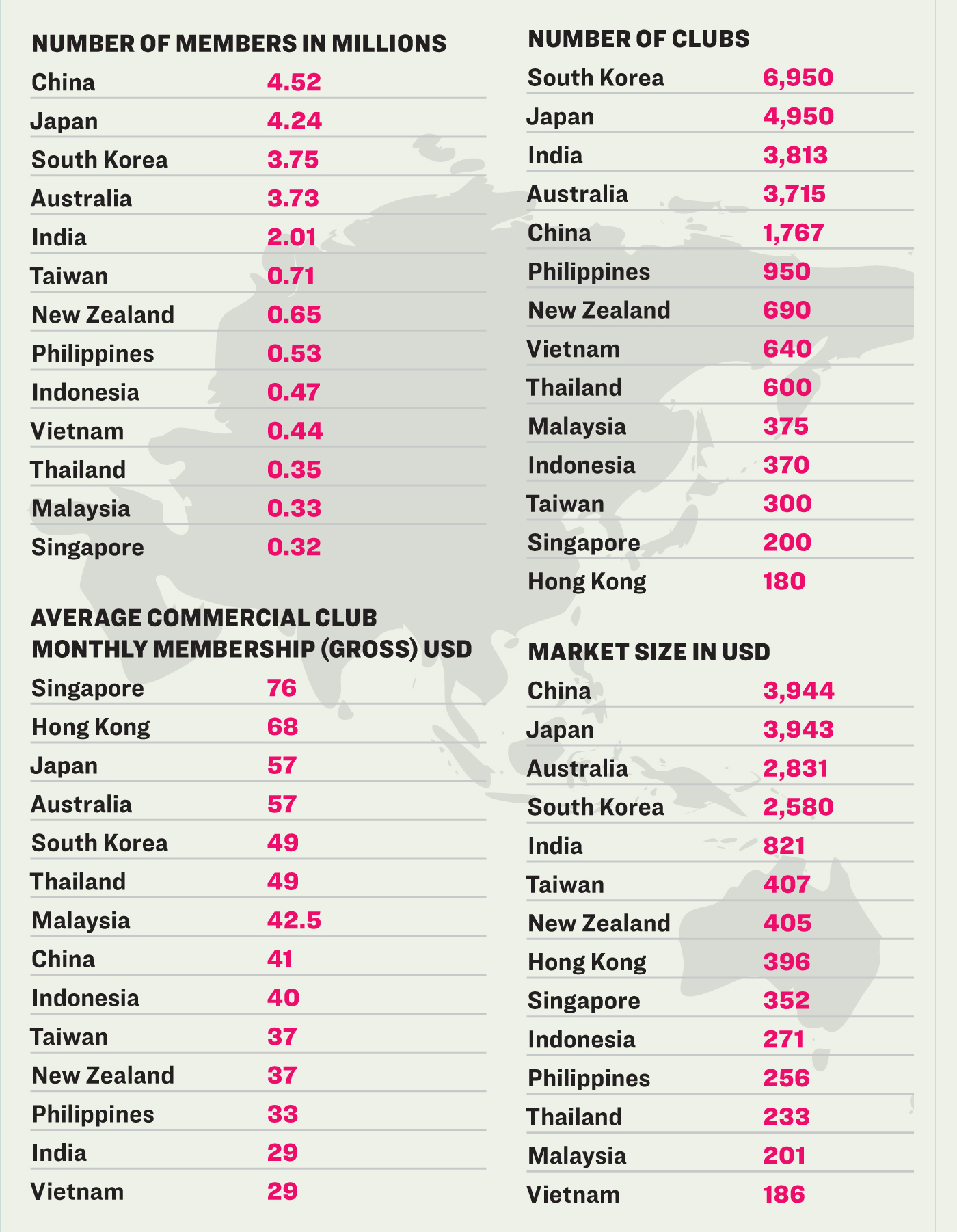

Deloitte says only two markets in the region are considered mature, these being Australia and New Zealand, which have the highest penetration rates at 15.3 per cent and 13.6 per cent, respectively.

While the fitness market shows signs of rapid growth and professionalisation in terms of penetration rates in Hong Kong (5.85 per cent), Singapore (5.8 per cent), and Japan (3.3 per cent), significant opportunities for growth still remain in less developmed markets, such as the Philippines (0.53 per cent), Thailand (0.5 per cent), Indonesia (0.18 per cent) and India (0.15 per cent).

Along with such growth opportunities come challenges. Real estate costs, limited rental availability, infrastructure underdevelopment, lack of professionalised services and increasing competition are just some of the realities club operators face when working in Asia-Pacific markets. However, a favourable economic outlook, along with increasing health awareness and demand for group exercise and personalised training, are expected to spur expansion.

“Driven by the momentum of economic prosperity, the fitness market in the Asia-Pacific region has shown steady growth, with a positive outlook going forward,” says Alan MacCharles, partner at Deloitte China. “Overall market penetration is on an upward trajectory, reflecting an increasing awareness of the importance of good health and the role a club membership can play in this.”

According to MacCharles, the region’s fitness market remains stratified due to varying stages of development, which can be categorised into three tiers.

Tier 1: Australia & New Zealand

Market penetration rates

Australia: 15.3 per cent

New Zealand: 13.6 per cent

These are relatively established markets, with higher penetration rates than their neighbours. However, the mature and professionalised markets in these countries indicate limited growth potential; labour and real estate costs have also constrained growth here.

Tier 2: Hong Kong, Singapore, Japan & Taiwan

Market penetration rates

Hong Kong: 5.85 per cent

Singapore: 5.8 per cent

Japan: 3.3 per cent

Taiwan: 3.0 per cent

These locations belong to the fast-expanding and maturing second-tier markets. This segment features gradually professionalising services, expanding consumer bases, and a high concentration of leading players.

With room for growth, already fierce competition is expected to continue in future in the Tier 2 region.

Tier 3: Rest of Asia-Pacific

Market penetration rates

Malaysia: 1.04 per cent

China’s top 10 cities: 0.97 per cent

Philippines: 0.53 per cent

Thailand: 0.5 per cent

Vietnam: 0.5 per cent

Indonesia: 0.18 per cent

India: 0.15 per cent

The remaining seven Asia-Pacific markets assessed by Deloitte are still in a comparatively early stage in their lifecycle, as a result of slower economic development and low awareness of personal health as a priority.

The fitness industry in these countries is typically concentrated in the respective capital cities and also the first-tier cities, where markets are mainly led by the larger, commercial fitness club chains.

The markets in second-tier cities are dominated by standalone players; mostly lower-end single site, independently owned operators – due to infrastructure underdevelopment, low purchasing power and low awareness of personalised training.

Underdeveloped regions in these countries demonstrate high growth potential, especially as rapid infrastructure development improves their accessibility and connectivity. Laws relating to the way gym contracts are configured also have an impact on the way each market develops. For example, in New Zealand (Tier 1) up-front payment for a long-term membership is forbidden by law, while in Singapore (Tier 2) some clubs collect one- and two-year contracts up-front.