Now in its fourth year, PwC’s Middle East Spa Benchmarking Survey focuses on spa performance and how facilities in the region can increase revenue. Mohammad Dahmash analyses the 2013 findings

By Mohammad Dahmash | Published in Spa Business Handbook 2014 issue 1

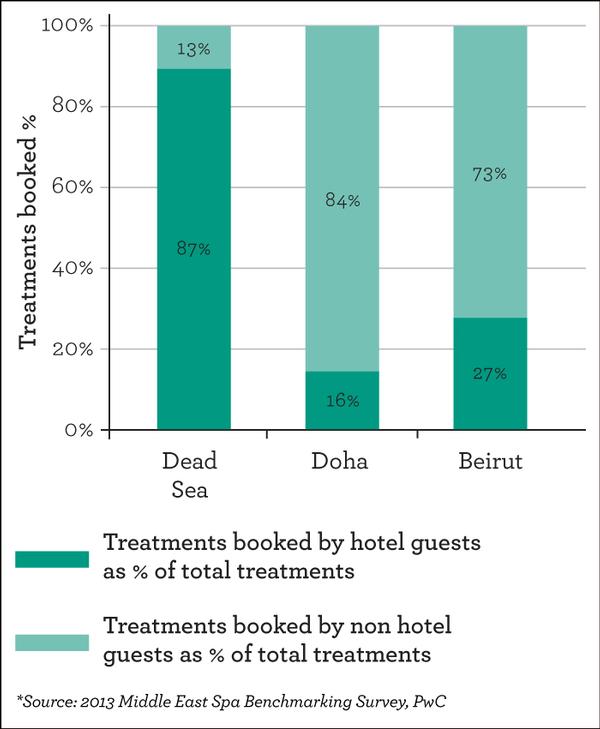

Graph 1: Treatments Booked by Hotel Guests vs Non Hotel Guests in 2013*

The Global Wellness Tourism Economy report estimates that the value of the wellness industry worldwide reached US$438.6bn (€315.8bn, £263.2bn) in 2013 (see p96). This is a staggering increase of more than 300 per cent in the past three years. Spas across the world and in the Middle East are looking to use this market to help improve their key performance indicators (KPIs).

The PricewaterhouseCoopers (PwC) Middle East Spa Benchmarking Survey was launched in January 2010 and focuses on three key spa markets in the Middle East: the Dead Sea region in Jordan, Doha in Qatar and Beirut in Lebanon.

The report, which is prepared on a quarterly basis, aims to provide spa/hotel operators, owners, investors, as well as hospitality developers with insight on the performance of the industry to drive operational decisions and increase profitability. It reviews 11 key performance metrics related to revenue across each spa market. All of its partner spas are attached to five-star hotels, and it requires a minimum of three spas in each market to preserve confidentiality of information.

Urban versus destination spa The 2013 Middle East Spa Benchmarking Survey is based on figures from last year and showed that majority of Dubai and Beirut spa treatments were booked by non-hotel guests (84 per cent and 73 per cent, respectively). In contrast, spa treatments booked by non-hotel guests only accounted for 13 per cent of treatments booked in Dead Sea spas (see Graph 1). This discrepancy is mainly due to the fact that spas in Doha and Beirut are located in vibrant urban settings and tend to cater to local populations instead of hotel guests, whereas spas in the Dead Sea area are primarily used by leisure and wellness tourists looking to escape noisy cities and experience the lake’s unique landscape.

Spas in urban settings such as in Beirut and Doha place a greater emphasis on attracting local customers over hotel guests to boost the bottom line. These spas usually rely on other revenue streams to increase profitability such as fitness and membership fees. Indeed, monies from fitness and membership accounted for more 54 per cent of total revenue in Doha hotel spas and 51 per cent in Beirut.

On the other hand, spas in the Dead Sea region didn’t generate any revenue from fitness and membership fees. The difference can be explained by the lack of an affluent population in the region surrounding the Dead Sea and by the fact that the destination resort attracts mainly tourists.

Spas in the Dead Sea region do have better retail revenue, however. They benefit from natural wellness/healing treatments stemming from the local hot springs and a wide range of products incorporate unique elements from the lake. It’s no surprise therefore that retail revenues, although undercapitalised in all three markets, are the highest in Dead Sea spas.

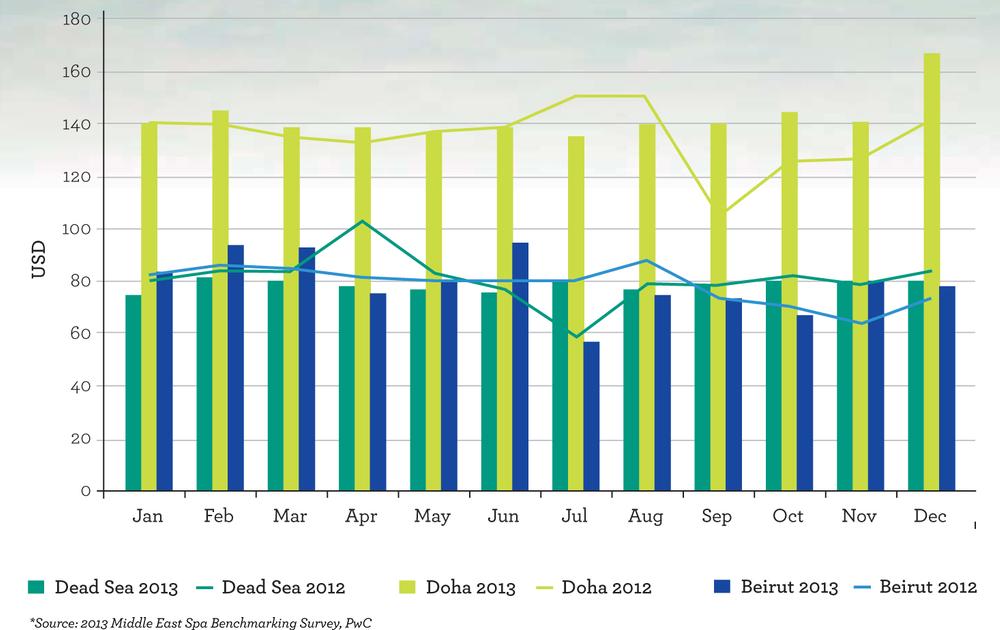

Average treatment revenue Doha is the second largest growing spa market in the Middle East after Dubai. Graph 2 shows that in 2013, the average treatment revenue per treatment sold in Doha spas was an astonishing 90 per cent higher than both Dead Sea and Beirut spas at US$142 (€102, £85) per treatment, recording an increase of 2.6 per cent from 2012. Additionally, spas in Beirut and the Dead Sea area recorded a 0.5 per cent and 6 per cent decrease, respectively, in average treatment revenue per treatment sold, which can be explained by the political instability in Lebanon and neighbouring countries – Jordan sits next to Syria and Iraq.

While average treatment revenue is useful in measuring spend per booking, spas need to be careful when relying on this KPI. An increase in cost might lead consumers to look elsewhere. To raise prices but not deter guests, spas could add a unique treatment that’s perceived as a higher-value service and that's different to what competitors offer. The Four Seasons in Doha, for example, offers tailored treatments with all-natural products and provides a different experience than any other spa in the city.

Revpath The revenue per available treatment hour (RevPATH) is one of the most important metrics for spas to track. It provides an insight into revenue management techniques and operational efficiency. Further, the RevPATH allows spa operators to identify patterns and peaks in demand during different times of the day which helps them to tailor their offering with different prices and promotions in order to capture more customers and increase their profits. This important tool captures a standardised assessment of spas using a universal attribute irrelevant of location and offering: time.

PwC’s analysis revealed that Doha spas recorded a RevPATH at US$25 (€18, £15) in 2013, the highest among the three markets in the survey. Some factors that might explain why spas have a hard time increasing RevPATH are a lack of available treatment rooms, low revenues, as well as an inability to attract more customers. Destination spas such as in the Dead Sea region, for example, can only attract tourists. Meanwhile urban spas have access to a bigger pool of potential customers because they can attract local, visitors who are more likely to return.

Therapist productivity Analysing therapist productivity is a key tool in determining whether a spa is generating enough demand. It also provides insight into a spa’s personnel management. A low utilisation of therapists’ hours, for example, can reflect a low demand for spa treatments as well as overstaffing. It’s very important for spa operators to increase their therapists’ productivity by creating a balance between periods of high and low demand to ensure that the facility is not overstaffed.

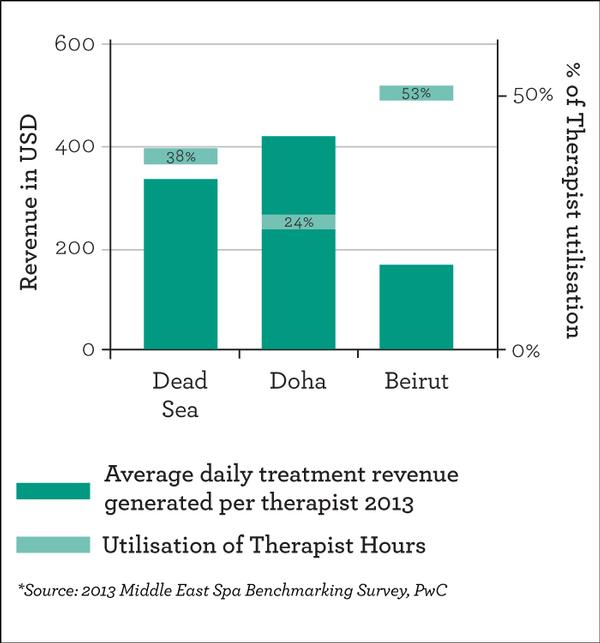

Graph 3 shows that while Doha accounted for the highest average daily treatment generated per therapist in 2013 –US$421 (€303, £253) – it reported the lowest utilisation of therapist hours in the three markets surveyed. This might be attributed to overstaffing and/or inefficient appointment scheduling.

The utilisation of therapists’ hours in Beirut spas increased by 27 per cent from 2012 to 2013, which is indicative of better staffing efficiency during that year coupled with better scheduling.

It’s interesting to note that, overall, almost less than half of all therapists’ hours were utilised in 2013. This could translate into a crucial area of improvement for the surveyed spas.

Gaining momentum On the whole, the Doha spa market experienced the strongest performance out of the three markets which were surveyed in 2013. Doha spas were more successful in attracting bookings and in generating treatment revenue.

Although the Beirut spa market seemed to suffer the most out of these markets – especially in terms of attracting customers and generating revenues – it’s worth noting that they were more successful at managing scheduling and therapist efficiency. Spas in this market recorded the highest utilisation of treatment room hours and therapists’ hours.

The Beirut market’s struggle to book revenue could have resulted from the country’s political instability. This has been linked to a drop in tourism and a slowdown of the economy, resulting in a decrease in hotel guests as well as leisure/wellness spending from the local population.

Overall, however, the spa industry is gaining momentum in the Middle East and is expected to grow over the next few years. The spas in PwC’s surveyed markets have an opportunity to improve their KPIs by placing more emphasis on staff and treatment room efficiency, implementing strategies to convert more hotel guests to spa customers, boosting retail sales and increasing the number of treatments booked by guests.

For a full copy of the 2013 PwC Middle East Spa Benchmarking Survey email [email protected]

Mohammad Dahmash is a partner of PwC’s real estate, hospitality and leisure advisory practice in Dubai. Prior to this, he led Ernst & Young’s real estate advisory group in the Middle East and Andersen’s real estate and hospitality group in the Middle East and North Africa, where he managed and supervised many of the landmark projects in the region.

The Spa Life UK Convention returns from 21–23 June 2026 at Whittlebury Park Hotel, Spa &

Golf Resort, bringing together spa managers, directors and owners for two days of focused

education, meaningful connection and commercial insight. [more...]

+ More featured suppliers

COMPANY PROFILES

Fenix Group srl

Fenix Group, founded by Gianluca Cavalletti in Italy, launched Endospheres to revolutionise aestheti [more...]

Nilo Spa Design

Nilo SPA Design, part of the Maletti group, has led the Beauty & Wellness sector for over 35 years p [more...]

Now in its fourth year, PwC’s Middle East Spa Benchmarking Survey focuses on spa performance and how facilities in the region can increase revenue. Mohammad Dahmash analyses the 2013 findings

By Mohammad Dahmash | Published in Spa Business Handbook 2014 issue 1

Graph 1: Treatments Booked by Hotel Guests vs Non Hotel Guests in 2013*

The Global Wellness Tourism Economy report estimates that the value of the wellness industry worldwide reached US$438.6bn (€315.8bn, £263.2bn) in 2013 (see p96). This is a staggering increase of more than 300 per cent in the past three years. Spas across the world and in the Middle East are looking to use this market to help improve their key performance indicators (KPIs).

The PricewaterhouseCoopers (PwC) Middle East Spa Benchmarking Survey was launched in January 2010 and focuses on three key spa markets in the Middle East: the Dead Sea region in Jordan, Doha in Qatar and Beirut in Lebanon.

The report, which is prepared on a quarterly basis, aims to provide spa/hotel operators, owners, investors, as well as hospitality developers with insight on the performance of the industry to drive operational decisions and increase profitability. It reviews 11 key performance metrics related to revenue across each spa market. All of its partner spas are attached to five-star hotels, and it requires a minimum of three spas in each market to preserve confidentiality of information.

Urban versus destination spa The 2013 Middle East Spa Benchmarking Survey is based on figures from last year and showed that majority of Dubai and Beirut spa treatments were booked by non-hotel guests (84 per cent and 73 per cent, respectively). In contrast, spa treatments booked by non-hotel guests only accounted for 13 per cent of treatments booked in Dead Sea spas (see Graph 1). This discrepancy is mainly due to the fact that spas in Doha and Beirut are located in vibrant urban settings and tend to cater to local populations instead of hotel guests, whereas spas in the Dead Sea area are primarily used by leisure and wellness tourists looking to escape noisy cities and experience the lake’s unique landscape.

Spas in urban settings such as in Beirut and Doha place a greater emphasis on attracting local customers over hotel guests to boost the bottom line. These spas usually rely on other revenue streams to increase profitability such as fitness and membership fees. Indeed, monies from fitness and membership accounted for more 54 per cent of total revenue in Doha hotel spas and 51 per cent in Beirut.

On the other hand, spas in the Dead Sea region didn’t generate any revenue from fitness and membership fees. The difference can be explained by the lack of an affluent population in the region surrounding the Dead Sea and by the fact that the destination resort attracts mainly tourists.

Spas in the Dead Sea region do have better retail revenue, however. They benefit from natural wellness/healing treatments stemming from the local hot springs and a wide range of products incorporate unique elements from the lake. It’s no surprise therefore that retail revenues, although undercapitalised in all three markets, are the highest in Dead Sea spas.

Average treatment revenue Doha is the second largest growing spa market in the Middle East after Dubai. Graph 2 shows that in 2013, the average treatment revenue per treatment sold in Doha spas was an astonishing 90 per cent higher than both Dead Sea and Beirut spas at US$142 (€102, £85) per treatment, recording an increase of 2.6 per cent from 2012. Additionally, spas in Beirut and the Dead Sea area recorded a 0.5 per cent and 6 per cent decrease, respectively, in average treatment revenue per treatment sold, which can be explained by the political instability in Lebanon and neighbouring countries – Jordan sits next to Syria and Iraq.

While average treatment revenue is useful in measuring spend per booking, spas need to be careful when relying on this KPI. An increase in cost might lead consumers to look elsewhere. To raise prices but not deter guests, spas could add a unique treatment that’s perceived as a higher-value service and that's different to what competitors offer. The Four Seasons in Doha, for example, offers tailored treatments with all-natural products and provides a different experience than any other spa in the city.

Revpath The revenue per available treatment hour (RevPATH) is one of the most important metrics for spas to track. It provides an insight into revenue management techniques and operational efficiency. Further, the RevPATH allows spa operators to identify patterns and peaks in demand during different times of the day which helps them to tailor their offering with different prices and promotions in order to capture more customers and increase their profits. This important tool captures a standardised assessment of spas using a universal attribute irrelevant of location and offering: time.

PwC’s analysis revealed that Doha spas recorded a RevPATH at US$25 (€18, £15) in 2013, the highest among the three markets in the survey. Some factors that might explain why spas have a hard time increasing RevPATH are a lack of available treatment rooms, low revenues, as well as an inability to attract more customers. Destination spas such as in the Dead Sea region, for example, can only attract tourists. Meanwhile urban spas have access to a bigger pool of potential customers because they can attract local, visitors who are more likely to return.

Therapist productivity Analysing therapist productivity is a key tool in determining whether a spa is generating enough demand. It also provides insight into a spa’s personnel management. A low utilisation of therapists’ hours, for example, can reflect a low demand for spa treatments as well as overstaffing. It’s very important for spa operators to increase their therapists’ productivity by creating a balance between periods of high and low demand to ensure that the facility is not overstaffed.

Graph 3 shows that while Doha accounted for the highest average daily treatment generated per therapist in 2013 –US$421 (€303, £253) – it reported the lowest utilisation of therapist hours in the three markets surveyed. This might be attributed to overstaffing and/or inefficient appointment scheduling.

The utilisation of therapists’ hours in Beirut spas increased by 27 per cent from 2012 to 2013, which is indicative of better staffing efficiency during that year coupled with better scheduling.

It’s interesting to note that, overall, almost less than half of all therapists’ hours were utilised in 2013. This could translate into a crucial area of improvement for the surveyed spas.

Gaining momentum On the whole, the Doha spa market experienced the strongest performance out of the three markets which were surveyed in 2013. Doha spas were more successful in attracting bookings and in generating treatment revenue.

Although the Beirut spa market seemed to suffer the most out of these markets – especially in terms of attracting customers and generating revenues – it’s worth noting that they were more successful at managing scheduling and therapist efficiency. Spas in this market recorded the highest utilisation of treatment room hours and therapists’ hours.

The Beirut market’s struggle to book revenue could have resulted from the country’s political instability. This has been linked to a drop in tourism and a slowdown of the economy, resulting in a decrease in hotel guests as well as leisure/wellness spending from the local population.

Overall, however, the spa industry is gaining momentum in the Middle East and is expected to grow over the next few years. The spas in PwC’s surveyed markets have an opportunity to improve their KPIs by placing more emphasis on staff and treatment room efficiency, implementing strategies to convert more hotel guests to spa customers, boosting retail sales and increasing the number of treatments booked by guests.

For a full copy of the 2013 PwC Middle East Spa Benchmarking Survey email [email protected]

Mohammad Dahmash is a partner of PwC’s real estate, hospitality and leisure advisory practice in Dubai. Prior to this, he led Ernst & Young’s real estate advisory group in the Middle East and Andersen’s real estate and hospitality group in the Middle East and North Africa, where he managed and supervised many of the landmark projects in the region.

Global Wellness Day (GWD) will mark its 15th anniversary on Saturday 13 June 2026, with the

theme: #JoyMagenta – a celebration of the healing qualities of simple gestures and activities

that spark joy.

Global luxury hospitality brand, Six Senses, has partnered with longevity healthcare provider,

HUM2N, to launch a clinic at Six Senses London, at The Whiteley.

As part of its first hotel partnership, Mayrlife – the medical health resort company known for its

site in Altaussee, Austria – has launched a day clinic at the Rosewood Vienna.

Premium London health club, KX Chelsea, will imminently unveil its most significant

redevelopment since its launch in 2002 to create an integrated wellness model combining

training, recovery and relaxation.

Rosewood Le Guanahani St Barth, on the northeast coast of Saint Barthélemy in the French

West Indies, is offering a programme of ocean-inspired yoga classes between 8-14 June to

celebrate Global Wellness Day (GWD).

Hotel de France, located on the British Isle of Jersey, has created a wellness retreat package

that includes a hot yoga session that will take place in Jersey Zoo’s butterfly sanctuary.

The Ritz-Carlton, Langkawi, in Malaysia, has revealed a schedule for Global Wellness Day

(GWD) that includes guided rainforest walks, mindful movement and guided coastal meditation

experiences.

Longevitix, a clinical platform for preventive and longevity medicine, has launched its AI-

powered intelligence system to help physicians deliver continuous, personalised longevity-

focused care at scale.

Atmantan Wellness Centre, an integrative wellness destination in Mulshi, near Pune in India, is

expanding its portfolio by adding a new centre in Hyderabad that will launch between 2028 and

2029.

A recent survey by the UK Spa Association (UKSA) into the industry’s approach to cancer care

has revealed that almost half of participating respondents (46 per cent) are unaware that

cancer is a disability and guests with a cancer diagnosis must be given

The Spa Life UK Convention returns from 21–23 June 2026 at Whittlebury Park Hotel, Spa &

Golf Resort, bringing together spa managers, directors and owners for two days of focused

education, meaningful connection and commercial insight. [more...]

+ More featured suppliers

COMPANY PROFILES

Fenix Group srl Fenix Group, founded by Gianluca Cavalletti in Italy, launched Endospheres to revolutionise aestheti [more...]