According to a report by PricewaterhouseCoopers (PwC), which looks at the global sports market towards 2015, global sports revenues will grow to US$145.3bn (£93bn, E109.3bn) at an annual compound growth rate (CAGR) of 3.7 per cent.

This is attributed to an improved economy, a rebound in TV advertising, the on-going migration of sports to pay TV and the resurgence of financial services and car companies interest in sponsorship.

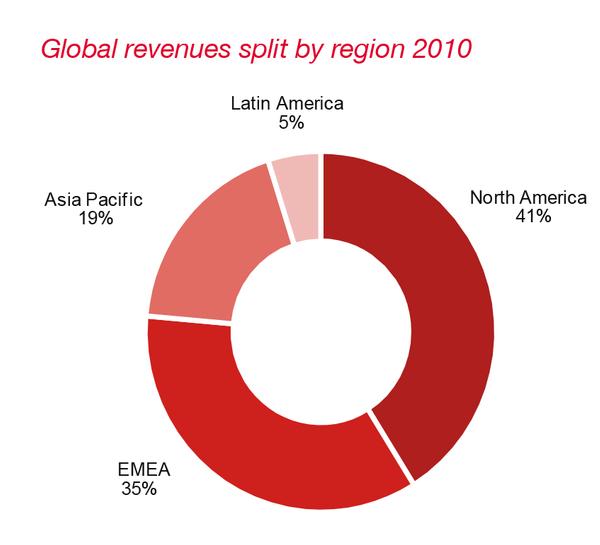

North America remains the largest market throughout PwC’s forecasts to 2015, followed by Europe; the Middle East and Africa (EMEA); and the Asian market. Latin America will remain the smallest market. Growth in the sports market in the BRIC countries (Brazil, Russia, India and China) strongly outpaced the overall global market during 2006 to 2010, but during the next five years this gap will narrow.

North America is still the largest market and growth rates will significantly outpace Asia Pacific and EMEA. While the balance of power is shifting to some emerging markets, which are hosting large-scale sports events over the next few years, the growth opportunities in the traditional developed markets are far from over.

Latin America is projected to have the highest growth rate at 4.9 per cent CAGR, partly due to the FIFA World Cup in Brazil in 2014, followed closely by North America at 4 per cent CAGR.

The EMEA is the second largest region with US$42.8bn (£27.4bn, E32.2bn) or 35 per cent of the total global revenues.

This region is projected to have the slowest growth rate at 2.9 per cent. This figure partly reflects the underlying economic conditions and is a reflection of the timing of major sports events, with 2010 being such a strong year in EMEA – given the South Africa FIFA World Cup – and 2015 being a relatively quiet year.

EMEA shows the most fluctuation over the period, given the 2012 London Olympic and Paralympic Games and the Football European Championships in Poland and Ukraine and then in 2014, the Winter Olympics in Sochi and the Commonwealth Games in Glasgow. If the impact of these one-off events is excluded, the underlying growth rate is 4.6 per cent.

What has been clear however, through this era of economic uncertainty, is that the balance of global economic power is shifting to the East and this will help maintain the internationalisation as sports seek new revenues from the growing middle classes in the emerging nations.

CONTINUAL GROWTH According to the report, despite the world’s troubled economic climate, the global sports industry has continued to thrive – with many major sporting events proving to be more popular than ever.

The popularity of these major events is supported by the on-going improvements in broadcasting and technology, which is allowing for better quality coverage than ever seen before. At the same time, television companies, sports clubs, governing bodies and even the sports stars themselves, are embracing social media to engage with fans and deliver to them a greater intensity of loyalty experience.

THE SPORTS INDUSTRY BY MARKET SEGMENTS Gate Revenues: Gate revenues will remain the biggest component of the global sports market. These account for 32.6 per cent of the total revenue (US$44.7 bn, £28.6bn, E33.6bn) in 2015. They’re particularly a key source of income in the regions where live sports events are part of the local culture. However, this mature market will see the lowest growth across all segments of the sports market at just 2.5 per cent CAGR from 2011-2015.

In EMEA, PwC expects modest growth, averaging less than 2 per cent, compounded annually during the next two years, with only slightly higher increases of just over 3 per cent annually for ongoing events during 2013–15. The gate revenue market is effectively saturated for the top events and record attendances have been witnessed at major events this year in the UK.

One unlikely area which could stimulate growth is regulation. In European football, The Union of European Football Associations (UEFA) financial fair play rules are forcing clubs to boost their revenues and are providing an extra impetus for new stadia development.

Changing the format of sporting events is also something which has been tried to make events more exciting and appealing to new audiences. For example, the England Hockey Board has recently announced the launch of Rush Hockey – an indoor or outdoor four- or five-a-side format.

Sponsorship: Accounting for 28.8 per cent of the total sports markets, sponsorship will see an average growth rate of 5.3 per cent to 2015. This will generate global revenues of US$45.3bn (£29bn, E34.1bn), which is split evenly across all regions.

The structure of sponsorship deals has changed. It’s no longer just about brand visibility and awareness, now it’s about gaining a deeper and more emotional engagement with fans and staff – something which some of the newly launched digital technologies are enabling.

Advertisers and sponsors are integrating social media into their sports involvement and through this and smart data mining, they are able to target their messages and content so that it’s relevant to each consumer segment and appropriate for each platform and delivery device.

Media Rights: Media rights is the third largest category of revenue and accounts for 24.1 per cent of the total market. It is the second fastest growing sector at 3.8 per cent CAGR. Revenues will see fairly healthy growth from US$29.2bn (£18.7bn, E21.9bn) in 2010 to US$35.2bn (£22.5bn, E26.5bn) in 2015. However, these figures mask large year-on-year swings, which reflect the traditionally dramatic impact of major global events held in ‘even’ years, such as the Olympics and FIFA World Cups.

Broadcasting still generates the majority of income from media rights, but engagement through different media platforms such as the internet and mobile phones can enhance and expand the fan’s experience. Smart use of social networking can add further value for both themselves and the user and many TV companies have invested in interactive portals. This enables them to combine online TV screening with social media, which complements their offering to the market.

Merchandising: Merchandising remains the smallest category of revenue – accounting for 14.5 per cent of total global revenue. However, it accounts for just over a quarter of all revenue in North America. Growth in merchandising revenue is closely linked with consumer spending patterns and overall growth is similar to gate revenues at 2.6 per cent CAGR, generating revenues of US$20.1bn (£12.9bn, E15.1bn) in 2015, up from US$17.6bn (£11.3bn, E13.2bn) in 2010.

Sports clubs are seeing a larger proportion of their merchandise transactions moving online, which allows them to engage and interact with fans who can’t attend matches – including those living in other countries. This engagement helps to promote sports brands in those regions and markets and builds demand for media coverage of the clubs involved.

LOOKING FORWARD With reference to what the future might hold for the sports market in a world of increasing economic and political uncertainty, PwC predicts the following: • Growth will come from the emerging sports markets in the BRIC countries and the Middle East, which will continue to offer scope for the development of new commercial opportunities – both in domestic and international sports events. • Sponsors will demand more sophisticated measurement techniques to demonstrate their return on investment. • Sports bodies and associations must, and will, introduce new regulations to control the cost base and levels of debt in their sports – to leave a sustainable business model for future generations. • Sports bodies must balance the increased commercial demands of their sports with the need to maintain the integrity and unpredictability that make sporting competitions so exciting and appealing to their supporters. • Across the world we’re seeing ever closer convergence between the sport and entertainment industries as both sectors rise to the challenges brought by digital technologies, which are changing and shaping the way we spend our leisure time. This new digital environment is significantly contributing to the globalisation of both the industry and specific sports.

Julie Clark leads the sport and leisure practice at PwC in the UK and is a member of PwC’s Global Hospitality and Leisure Practice. She advises governments and investors on major events and capital projects.

According to a report by PricewaterhouseCoopers (PwC), which looks at the global sports market towards 2015, global sports revenues will grow to US$145.3bn (£93bn, E109.3bn) at an annual compound growth rate (CAGR) of 3.7 per cent.

This is attributed to an improved economy, a rebound in TV advertising, the on-going migration of sports to pay TV and the resurgence of financial services and car companies interest in sponsorship.

North America remains the largest market throughout PwC’s forecasts to 2015, followed by Europe; the Middle East and Africa (EMEA); and the Asian market. Latin America will remain the smallest market. Growth in the sports market in the BRIC countries (Brazil, Russia, India and China) strongly outpaced the overall global market during 2006 to 2010, but during the next five years this gap will narrow.

North America is still the largest market and growth rates will significantly outpace Asia Pacific and EMEA. While the balance of power is shifting to some emerging markets, which are hosting large-scale sports events over the next few years, the growth opportunities in the traditional developed markets are far from over.

Latin America is projected to have the highest growth rate at 4.9 per cent CAGR, partly due to the FIFA World Cup in Brazil in 2014, followed closely by North America at 4 per cent CAGR.

The EMEA is the second largest region with US$42.8bn (£27.4bn, E32.2bn) or 35 per cent of the total global revenues.

This region is projected to have the slowest growth rate at 2.9 per cent. This figure partly reflects the underlying economic conditions and is a reflection of the timing of major sports events, with 2010 being such a strong year in EMEA – given the South Africa FIFA World Cup – and 2015 being a relatively quiet year.

EMEA shows the most fluctuation over the period, given the 2012 London Olympic and Paralympic Games and the Football European Championships in Poland and Ukraine and then in 2014, the Winter Olympics in Sochi and the Commonwealth Games in Glasgow. If the impact of these one-off events is excluded, the underlying growth rate is 4.6 per cent.

What has been clear however, through this era of economic uncertainty, is that the balance of global economic power is shifting to the East and this will help maintain the internationalisation as sports seek new revenues from the growing middle classes in the emerging nations.

CONTINUAL GROWTH According to the report, despite the world’s troubled economic climate, the global sports industry has continued to thrive – with many major sporting events proving to be more popular than ever.

The popularity of these major events is supported by the on-going improvements in broadcasting and technology, which is allowing for better quality coverage than ever seen before. At the same time, television companies, sports clubs, governing bodies and even the sports stars themselves, are embracing social media to engage with fans and deliver to them a greater intensity of loyalty experience.

THE SPORTS INDUSTRY BY MARKET SEGMENTS Gate Revenues: Gate revenues will remain the biggest component of the global sports market. These account for 32.6 per cent of the total revenue (US$44.7 bn, £28.6bn, E33.6bn) in 2015. They’re particularly a key source of income in the regions where live sports events are part of the local culture. However, this mature market will see the lowest growth across all segments of the sports market at just 2.5 per cent CAGR from 2011-2015.

In EMEA, PwC expects modest growth, averaging less than 2 per cent, compounded annually during the next two years, with only slightly higher increases of just over 3 per cent annually for ongoing events during 2013–15. The gate revenue market is effectively saturated for the top events and record attendances have been witnessed at major events this year in the UK.

One unlikely area which could stimulate growth is regulation. In European football, The Union of European Football Associations (UEFA) financial fair play rules are forcing clubs to boost their revenues and are providing an extra impetus for new stadia development.

Changing the format of sporting events is also something which has been tried to make events more exciting and appealing to new audiences. For example, the England Hockey Board has recently announced the launch of Rush Hockey – an indoor or outdoor four- or five-a-side format.

Sponsorship: Accounting for 28.8 per cent of the total sports markets, sponsorship will see an average growth rate of 5.3 per cent to 2015. This will generate global revenues of US$45.3bn (£29bn, E34.1bn), which is split evenly across all regions.

The structure of sponsorship deals has changed. It’s no longer just about brand visibility and awareness, now it’s about gaining a deeper and more emotional engagement with fans and staff – something which some of the newly launched digital technologies are enabling.

Advertisers and sponsors are integrating social media into their sports involvement and through this and smart data mining, they are able to target their messages and content so that it’s relevant to each consumer segment and appropriate for each platform and delivery device.

Media Rights: Media rights is the third largest category of revenue and accounts for 24.1 per cent of the total market. It is the second fastest growing sector at 3.8 per cent CAGR. Revenues will see fairly healthy growth from US$29.2bn (£18.7bn, E21.9bn) in 2010 to US$35.2bn (£22.5bn, E26.5bn) in 2015. However, these figures mask large year-on-year swings, which reflect the traditionally dramatic impact of major global events held in ‘even’ years, such as the Olympics and FIFA World Cups.

Broadcasting still generates the majority of income from media rights, but engagement through different media platforms such as the internet and mobile phones can enhance and expand the fan’s experience. Smart use of social networking can add further value for both themselves and the user and many TV companies have invested in interactive portals. This enables them to combine online TV screening with social media, which complements their offering to the market.

Merchandising: Merchandising remains the smallest category of revenue – accounting for 14.5 per cent of total global revenue. However, it accounts for just over a quarter of all revenue in North America. Growth in merchandising revenue is closely linked with consumer spending patterns and overall growth is similar to gate revenues at 2.6 per cent CAGR, generating revenues of US$20.1bn (£12.9bn, E15.1bn) in 2015, up from US$17.6bn (£11.3bn, E13.2bn) in 2010.

Sports clubs are seeing a larger proportion of their merchandise transactions moving online, which allows them to engage and interact with fans who can’t attend matches – including those living in other countries. This engagement helps to promote sports brands in those regions and markets and builds demand for media coverage of the clubs involved.

LOOKING FORWARD With reference to what the future might hold for the sports market in a world of increasing economic and political uncertainty, PwC predicts the following: • Growth will come from the emerging sports markets in the BRIC countries and the Middle East, which will continue to offer scope for the development of new commercial opportunities – both in domestic and international sports events. • Sponsors will demand more sophisticated measurement techniques to demonstrate their return on investment. • Sports bodies and associations must, and will, introduce new regulations to control the cost base and levels of debt in their sports – to leave a sustainable business model for future generations. • Sports bodies must balance the increased commercial demands of their sports with the need to maintain the integrity and unpredictability that make sporting competitions so exciting and appealing to their supporters. • Across the world we’re seeing ever closer convergence between the sport and entertainment industries as both sectors rise to the challenges brought by digital technologies, which are changing and shaping the way we spend our leisure time. This new digital environment is significantly contributing to the globalisation of both the industry and specific sports.

Julie Clark leads the sport and leisure practice at PwC in the UK and is a member of PwC’s Global Hospitality and Leisure Practice. She advises governments and investors on major events and capital projects.

Global Wellness Day (GWD) marked its 15th anniversary on Saturday 13 June 2026, with the

theme: #JoyMagenta – a celebration of the healing qualities of simple gestures and activities

that spark joy.

Global luxury hospitality brand, Six Senses, has partnered with longevity healthcare provider,

HUM2N, to launch a clinic at Six Senses London, at The Whiteley.

As part of its first hotel partnership, Mayrlife – the medical health resort company known for its

site in Altaussee, Austria – has launched a day clinic at the Rosewood Vienna.

Premium London health club, KX Chelsea, will imminently unveil its most significant

redevelopment since its launch in 2002 to create an integrated wellness model combining

training, recovery and relaxation.

Rosewood Le Guanahani St Barth, on the northeast coast of Saint Barthélemy in the French

West Indies, is offering a programme of ocean-inspired yoga classes between 8-14 June to

celebrate Global Wellness Day (GWD).

Hotel de France, located on the British Isle of Jersey, has created a wellness retreat package

that includes a hot yoga session that will take place in Jersey Zoo’s butterfly sanctuary.

The Ritz-Carlton, Langkawi, in Malaysia, has revealed a schedule for Global Wellness Day

(GWD) that includes guided rainforest walks, mindful movement and guided coastal meditation

experiences.

Longevitix, a clinical platform for preventive and longevity medicine, has launched its AI-

powered intelligence system to help physicians deliver continuous, personalised longevity-

focused care at scale.

Atmantan Wellness Centre, an integrative wellness destination in Mulshi, near Pune in India, is

expanding its portfolio by adding a new centre in Hyderabad that will launch between 2028 and

2029.