Yes! Send me the FREE digital editions of Spa Business and Spa Business insider magazines and the FREE weekly Spa Business and Spa Business insider ezines and breaking news alerts!

Hotels with Major Wellness offerings are outperforming others, but bottom-line results were more varied. Roger Allen shares the highlights of the latest RLA Global Wellness Real Estate Report

Africa and the Middle East showed double-digit growth last year / shutterstock/Yiistocking

Wellness hotels of all sizes outperformed No Wellness hotels in revenue generation globally in 2024, according to the latest Wellness Real Estate Report by hospitality advisory RLA Global, produced in partnership with P&L benchmarking firm HotStats. Properties incorporating significant wellness amenities stood out in absolute top-line performance across the board and recorded a robust growth rate in the Upscale asset class.

The report, covering over 11,000 hotels worldwide, also found that occupancy remained largely stable in all categories last year, but ancillary on-site spending was somewhat lower than a year earlier and most properties couldn’t improve per-room food and beverage performance in 2024 – except for hotels with extensive wellness offerings. These properties also took the lead in revenue and profit generation in the leisure department.

Major Wellness hotels came roaring back in 2024, displaying a standout top-line performance in total revenue per available room (TRevPAR) and impressive year-on-year growth rates in the Upscale category. Minor Wellness hotels had higher growth in gross operating profit per room (GOPPAR), but Major Wellness assets outperformed them in GOPPAR in absolute terms.

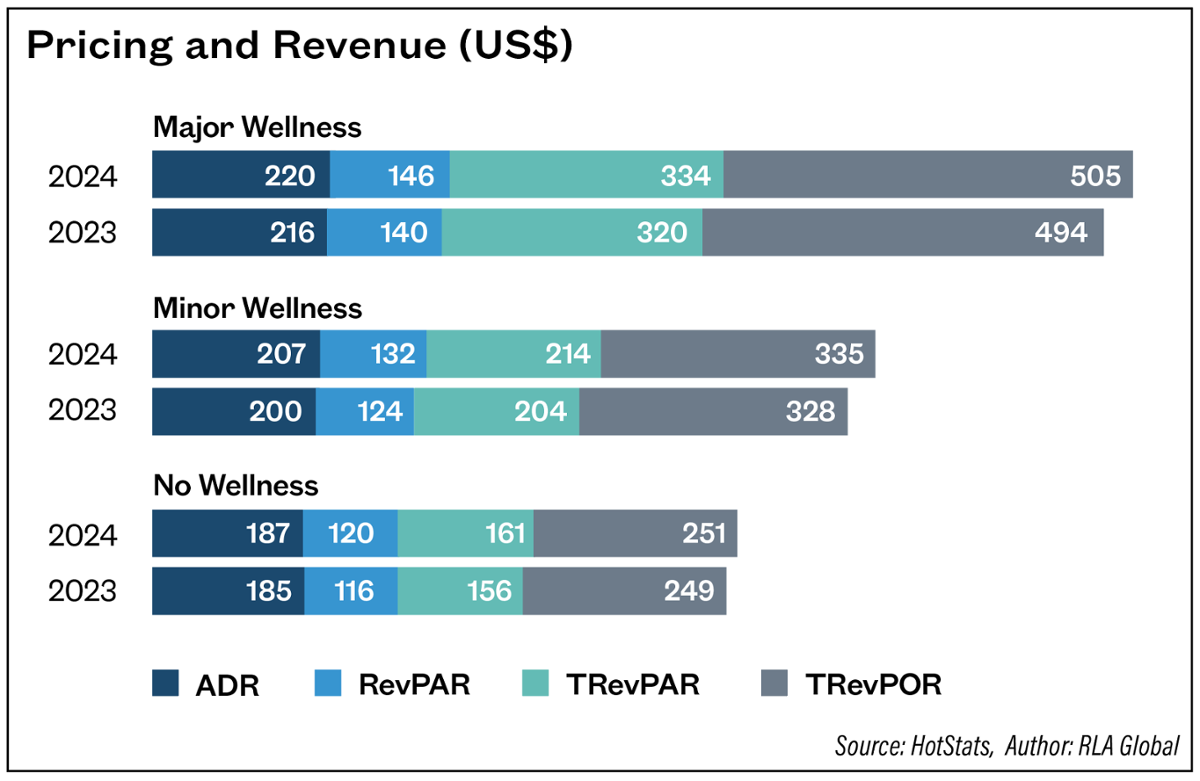

Wellness impact on hotel revenue Looking at top-line performances in more detail, the report shows that average TRevPAR at Major Wellness hotels was 56 per cent higher than at their Minor peers and a whopping 108 per cent above that of No Wellness hotels. This gap was also well pronounced in other revenue and pricing KPIs, such as daily room rates (ADR) and total revenue per occupied room (TRevPOR).

Minor Wellness properties had the highest year-on-year TRevPAR growth at 6 per cent last year, although Major Wellness hotels showed massive growth of up to 160 per cent in all revenue KPIs in the Upscale asset class.

In an example of striking results in the Upscale segment, the average total revenue per occupied room (TRevPOR) of Major Wellness hotels climbed to US$1,159 (€1001, £853) – by far the highest in any wellness category or asset class last year, up from just US$483 (€417, £356) in 2023.

As Rachael Rothman, head of hotels research and data analytics at CBRE said: “Major Wellness assets in the Upscale segment are now outperforming even Luxury properties in total revenue per room – a clear sign that traditional assumptions about service levels and positioning are being challenged. This shift could have significant implications for how capital is allocated and how future developments are designed.”

All geographical markets displayed significant year-on-year improvement in TRevPAR last year. Africa and the Middle East had double-digit growth, with 10 per cent to 11 per cent growth in the Minor Wellness hotel category. European properties increased their TRevPAR by 6 per cent on average in all categories, while the Americas mostly recorded muted growth, ranging between 3 per cent and 5 per cent, and had a 1 per cent decline in the Major Wellness category.

While revenue performances indicate a mostly positive global trend, GOPPAR results remain modest, implying that TRevPAR growth doesn’t match cost increases and inflation. Profitability varies wildly, depending on region – for example, Africa achieved a double-digit GOPPAR growth last year, but the Americas had limited growth and recorded a 7 per cent drop in GOPPAR in the Major Wellness hotel category over the same period.

Unlocking more on-site spending Hotels with extensive wellness facilities and services tend to rely more on non-room revenue. Major Wellness properties drove 56 per cent of their TRevPAR from such ancillary income in 2024, while Minor Wellness had a more balanced revenue mix, with ancillary revenues accounting for 38 per cent of TRevPAR. This was just 24 per cent at No Wellness hotels.

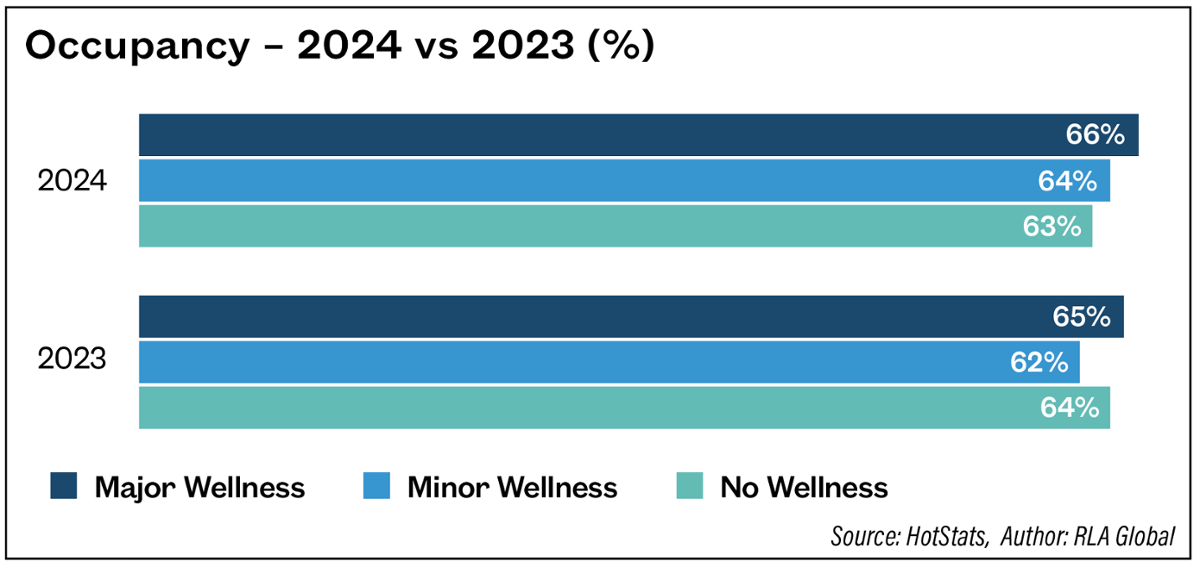

Room occupancy remained largely unchanged from a year earlier in all three hotel categories, and Michael Grove, CEO of HotStats, explains that while occupancy is holding steady – showing that travel demand remains strong – hotels can’t just ride the wave anymore. “With revenue growth starting to soften, the real challenge is unlocking more on-property spend, especially in wellness, where guest demand is high but monetisation still lags,” he said.

Occupancy follows seasonal patterns, which usually affect Major Wellness hotels the least, as their non-room and wellness offerings remain attractive and help drive occupancy even in the low and off seasons. The seasonality impact – or the gap between the highest and lowest occupancy periods – was the biggest at 13 percentage points at No Wellness properties.

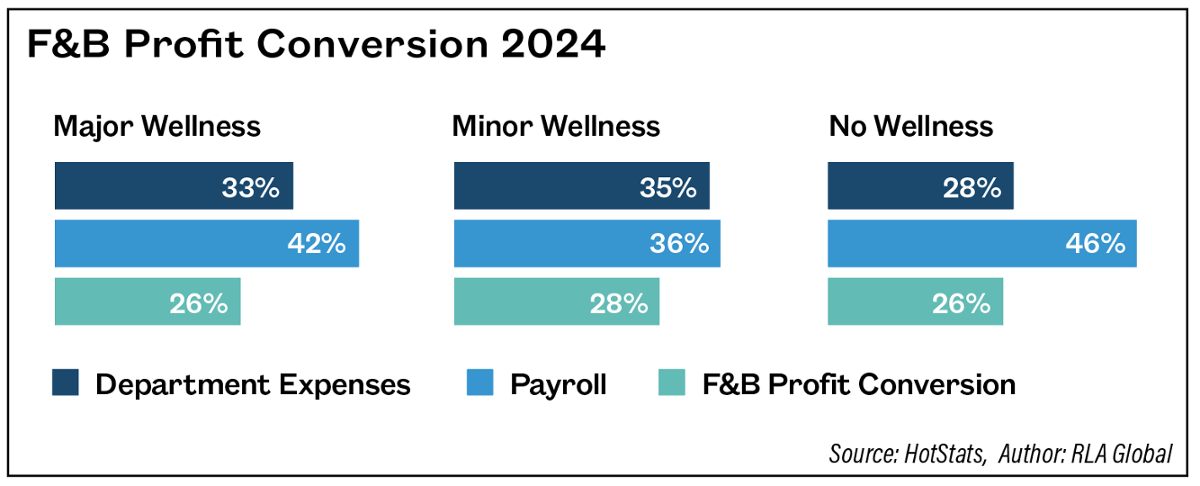

Leisure and F&B department trends The Wellness Real Estate Report also had interesting findings about leisure and F&B department performances in different hotel categories. Generally speaking, Major Wellness demonstrates a more profitable structure in leisure, maintaining lower payroll and departmental costs than Minor Wellness properties, which struggle with higher payroll. Major Wellness hotels had a healthy leisure performance last year with a profit conversion of 49 per cent. Payroll represents 35 per cent of their leisure income, suggesting significant staff requirements, but departmental expenses are minimal at 16 per cent, reflecting efficient operational spending. Minor Wellness hotels are constrained by high payroll, at 48 per cent of income in average, which impacts the bottom-line. Their departmental costs were at 20 per cent.

In the F&B segment, Major Wellness was the only group that could increase revenue per occupied room in 2024, but just by 1 per cent – suggesting that TRevPAR is mainly driven by the rooms and leisure departments. F&B revenue at No Wellness hotel is just half of that of their major counterparts, as No Wellness F&B offerings are typically limited.

As wellness offerings evolve, it’s clear that operational efficiency and targeted F&B concepts in Minor Wellness properties are driving profitability, while Major Wellness must look beyond traditional offerings to sustain growth.

One notable report finding that can potentially shape future F&B services is that room service had a very limited role in all categories last year, accounting for 1.3 per cent of total F&B revenue at Major Wellness hotels, 1.5 per cent at Minor Wellness properties and just 0.7 per cent at No Wellness hotels.

Effects on the bottom line vary The effects of wellness operations on the overall profitability of hotels on the property level show considerable variations, partially depending on the asset class. Major Wellness properties, for example, enjoyed a robust 63.8 per cent rise in GOPPAR in the Upscale hotel category, but faced GOPPAR declines of 3.3 per cent and 0.24 per cent in the Upper Upscale and Luxury categories, respectively. Overall, Major Wellness properties had 16 per cent higher average GOPPAR in absolute terms compared to their Minor peers. This difference was even bigger at 37 per cent when compared to No Wellness hotels. But Minor Wellness took the lead in GOPPAR growth in 2024, with an average year-on-year rise of 5 per cent, well exceeding 1 per cent and 2 per cent in the Major Wellness and No Wellness segments.

Minor Wellness continues to surpass Major Wellness in both total profit conversion and gross operating profit rates, reinforcing its status as the most profit-driven category. Meanwhile, chain-scale performance highlights Major Wellness achieving an impressive year-on-year growth in GOPPAR, suggesting that wellness profitability – and consequently demand – is strong within more economically positioned hotels.

Terminologies used:

Major Wellness Hotels: Wellness and Leisure Revenue annually exceeding US$1m or more than 10% of total hotel revenues.

Minor Wellness Hotels: Wellness and Leisure Revenue annually achieving less than US$1m or less than 10% of total hotel revenues.

No Wellness Hotels: No Wellness-related income.

For more market data and insights, download the 2025 Wellness Real Estate Report for free at WellnessRealEstateReport.com

■ About the author:

RLA GLOBAL

Roger A. Allen is group CEO of RLA Global, a boutique advisory firm that specialises in hospitality and tourism assets that are strongly influenced by leisure, entertainment, wellbeing and retail.

Le Atelier by C.O.D.E. doesn't offer a standard bespoke service, it provides a highly

customised approach to designing massage beds and loungers in high-end wellness

environments. [more...]

Hotels with Major Wellness offerings are outperforming others, but bottom-line results were more varied. Roger Allen shares the highlights of the latest RLA Global Wellness Real Estate Report

Africa and the Middle East showed double-digit growth last year / shutterstock/Yiistocking

Wellness hotels of all sizes outperformed No Wellness hotels in revenue generation globally in 2024, according to the latest Wellness Real Estate Report by hospitality advisory RLA Global, produced in partnership with P&L benchmarking firm HotStats. Properties incorporating significant wellness amenities stood out in absolute top-line performance across the board and recorded a robust growth rate in the Upscale asset class.

The report, covering over 11,000 hotels worldwide, also found that occupancy remained largely stable in all categories last year, but ancillary on-site spending was somewhat lower than a year earlier and most properties couldn’t improve per-room food and beverage performance in 2024 – except for hotels with extensive wellness offerings. These properties also took the lead in revenue and profit generation in the leisure department.

Major Wellness hotels came roaring back in 2024, displaying a standout top-line performance in total revenue per available room (TRevPAR) and impressive year-on-year growth rates in the Upscale category. Minor Wellness hotels had higher growth in gross operating profit per room (GOPPAR), but Major Wellness assets outperformed them in GOPPAR in absolute terms.

Wellness impact on hotel revenue Looking at top-line performances in more detail, the report shows that average TRevPAR at Major Wellness hotels was 56 per cent higher than at their Minor peers and a whopping 108 per cent above that of No Wellness hotels. This gap was also well pronounced in other revenue and pricing KPIs, such as daily room rates (ADR) and total revenue per occupied room (TRevPOR).

Minor Wellness properties had the highest year-on-year TRevPAR growth at 6 per cent last year, although Major Wellness hotels showed massive growth of up to 160 per cent in all revenue KPIs in the Upscale asset class.

In an example of striking results in the Upscale segment, the average total revenue per occupied room (TRevPOR) of Major Wellness hotels climbed to US$1,159 (€1001, £853) – by far the highest in any wellness category or asset class last year, up from just US$483 (€417, £356) in 2023.

As Rachael Rothman, head of hotels research and data analytics at CBRE said: “Major Wellness assets in the Upscale segment are now outperforming even Luxury properties in total revenue per room – a clear sign that traditional assumptions about service levels and positioning are being challenged. This shift could have significant implications for how capital is allocated and how future developments are designed.”

All geographical markets displayed significant year-on-year improvement in TRevPAR last year. Africa and the Middle East had double-digit growth, with 10 per cent to 11 per cent growth in the Minor Wellness hotel category. European properties increased their TRevPAR by 6 per cent on average in all categories, while the Americas mostly recorded muted growth, ranging between 3 per cent and 5 per cent, and had a 1 per cent decline in the Major Wellness category.

While revenue performances indicate a mostly positive global trend, GOPPAR results remain modest, implying that TRevPAR growth doesn’t match cost increases and inflation. Profitability varies wildly, depending on region – for example, Africa achieved a double-digit GOPPAR growth last year, but the Americas had limited growth and recorded a 7 per cent drop in GOPPAR in the Major Wellness hotel category over the same period.

Unlocking more on-site spending Hotels with extensive wellness facilities and services tend to rely more on non-room revenue. Major Wellness properties drove 56 per cent of their TRevPAR from such ancillary income in 2024, while Minor Wellness had a more balanced revenue mix, with ancillary revenues accounting for 38 per cent of TRevPAR. This was just 24 per cent at No Wellness hotels.

Room occupancy remained largely unchanged from a year earlier in all three hotel categories, and Michael Grove, CEO of HotStats, explains that while occupancy is holding steady – showing that travel demand remains strong – hotels can’t just ride the wave anymore. “With revenue growth starting to soften, the real challenge is unlocking more on-property spend, especially in wellness, where guest demand is high but monetisation still lags,” he said.

Occupancy follows seasonal patterns, which usually affect Major Wellness hotels the least, as their non-room and wellness offerings remain attractive and help drive occupancy even in the low and off seasons. The seasonality impact – or the gap between the highest and lowest occupancy periods – was the biggest at 13 percentage points at No Wellness properties.

Leisure and F&B department trends The Wellness Real Estate Report also had interesting findings about leisure and F&B department performances in different hotel categories. Generally speaking, Major Wellness demonstrates a more profitable structure in leisure, maintaining lower payroll and departmental costs than Minor Wellness properties, which struggle with higher payroll. Major Wellness hotels had a healthy leisure performance last year with a profit conversion of 49 per cent. Payroll represents 35 per cent of their leisure income, suggesting significant staff requirements, but departmental expenses are minimal at 16 per cent, reflecting efficient operational spending. Minor Wellness hotels are constrained by high payroll, at 48 per cent of income in average, which impacts the bottom-line. Their departmental costs were at 20 per cent.

In the F&B segment, Major Wellness was the only group that could increase revenue per occupied room in 2024, but just by 1 per cent – suggesting that TRevPAR is mainly driven by the rooms and leisure departments. F&B revenue at No Wellness hotel is just half of that of their major counterparts, as No Wellness F&B offerings are typically limited.

As wellness offerings evolve, it’s clear that operational efficiency and targeted F&B concepts in Minor Wellness properties are driving profitability, while Major Wellness must look beyond traditional offerings to sustain growth.

One notable report finding that can potentially shape future F&B services is that room service had a very limited role in all categories last year, accounting for 1.3 per cent of total F&B revenue at Major Wellness hotels, 1.5 per cent at Minor Wellness properties and just 0.7 per cent at No Wellness hotels.

Effects on the bottom line vary The effects of wellness operations on the overall profitability of hotels on the property level show considerable variations, partially depending on the asset class. Major Wellness properties, for example, enjoyed a robust 63.8 per cent rise in GOPPAR in the Upscale hotel category, but faced GOPPAR declines of 3.3 per cent and 0.24 per cent in the Upper Upscale and Luxury categories, respectively. Overall, Major Wellness properties had 16 per cent higher average GOPPAR in absolute terms compared to their Minor peers. This difference was even bigger at 37 per cent when compared to No Wellness hotels. But Minor Wellness took the lead in GOPPAR growth in 2024, with an average year-on-year rise of 5 per cent, well exceeding 1 per cent and 2 per cent in the Major Wellness and No Wellness segments.

Minor Wellness continues to surpass Major Wellness in both total profit conversion and gross operating profit rates, reinforcing its status as the most profit-driven category. Meanwhile, chain-scale performance highlights Major Wellness achieving an impressive year-on-year growth in GOPPAR, suggesting that wellness profitability – and consequently demand – is strong within more economically positioned hotels.

Terminologies used:

Major Wellness Hotels: Wellness and Leisure Revenue annually exceeding US$1m or more than 10% of total hotel revenues.

Minor Wellness Hotels: Wellness and Leisure Revenue annually achieving less than US$1m or less than 10% of total hotel revenues.

No Wellness Hotels: No Wellness-related income.

For more market data and insights, download the 2025 Wellness Real Estate Report for free at WellnessRealEstateReport.com

■ About the author:

RLA GLOBAL

Roger A. Allen is group CEO of RLA Global, a boutique advisory firm that specialises in hospitality and tourism assets that are strongly influenced by leisure, entertainment, wellbeing and retail.

Premium London health club, KX Chelsea, will imminently unveil its most significant

redevelopment since its launch in 2002 to create an integrated wellness model combining

training, recovery and relaxation.

Rosewood Le Guanahani St Barth, on the northeast coast of Saint Barthélemy in the French

West Indies, is offering a programme of ocean-inspired yoga classes between 8-14 June to

celebrate Global Wellness Day (GWD).

Hotel de France, located on the British Isle of Jersey, has created a wellness retreat package

that includes a hot yoga session that will take place in Jersey Zoo’s butterfly sanctuary.

The Ritz-Carlton, Langkawi, in Malaysia, has revealed a schedule for Global Wellness Day

(GWD) that includes guided rainforest walks, mindful movement and guided coastal meditation

experiences.

Longevitix, a clinical platform for preventive and longevity medicine, has launched its AI-

powered intelligence system to help physicians deliver continuous, personalised longevity-

focused care at scale.

Atmantan Wellness Centre, an integrative wellness destination in Mulshi, near Pune in India, is

expanding its portfolio by adding a new centre in Hyderabad that will launch between 2028 and

2029.

A recent survey by the UK Spa Association (UKSA) into the industry’s approach to cancer care

has revealed that almost half of participating respondents (46 per cent) are unaware that

cancer is a disability and guests with a cancer diagnosis must be given

Mexican operator, Solmar Hotels and Resorts, is hosting a series of events in celebration of

Global Wellness Day, including a Temazcal ceremony at its Playa Grande Resort and Spa in Los

Cabos.

Mandarin Oriental has announced a standalone residence brand, Mansions, which will debut at

Emirates Palace, Mandarin Oriental Mansions, Abu Dhabi, in 2029.

Le Atelier by C.O.D.E. doesn't offer a standard bespoke service, it provides a highly

customised approach to designing massage beds and loungers in high-end wellness

environments. [more...]