Yes! Send me the FREE digital editions of Spa Business and Spa Business insider magazines and the FREE weekly Spa Business and Spa Business insider ezines and breaking news alerts!

The TEA/AECOM 2014 Theme and Museum Index

indicates healthy attendance growth across all

regions, powered by the economic climate,

good weather and investment in new attractions

Aquaventure in Dubai atttracted 1.4 million visitors in 2014

The TEA/AECOM Theme and Museum Index is a collaboration of the Themed Entertainment Association (TEA) and the economics practice at AECOM, a global provider of technical-professional and management-support services.

The annual calendar-year study of global attractions attendance is a free resource for park operators, land developers and the travel industry. Top worldwide theme parks, amusement parks, waterparks, museums and theme park group operators are named and ranked by attendance, and industry trends are identified. The global market is studied as a whole, and each main region is also studied separately: the Americas, Europe and Asia. There’s also a table of the top waterparks in the world and in the US, and of the top global chain operators.

Here, AECOM looks at the numbers and makes comparisons with the 2009 listings.

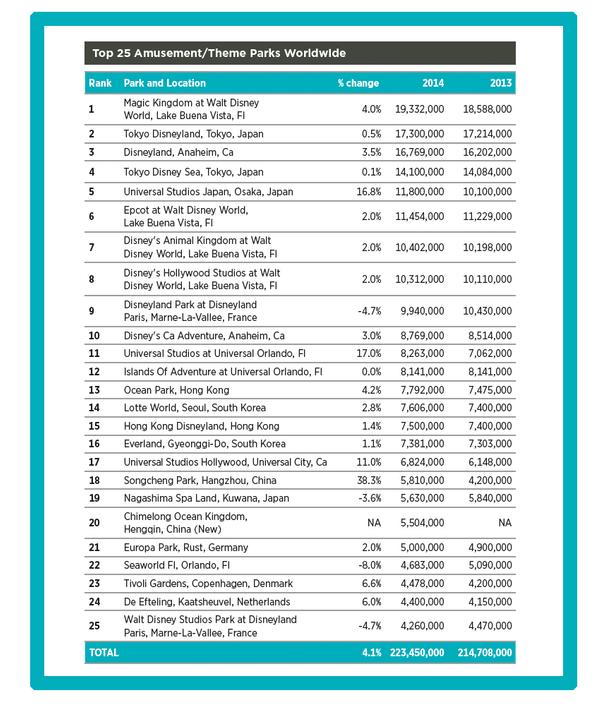

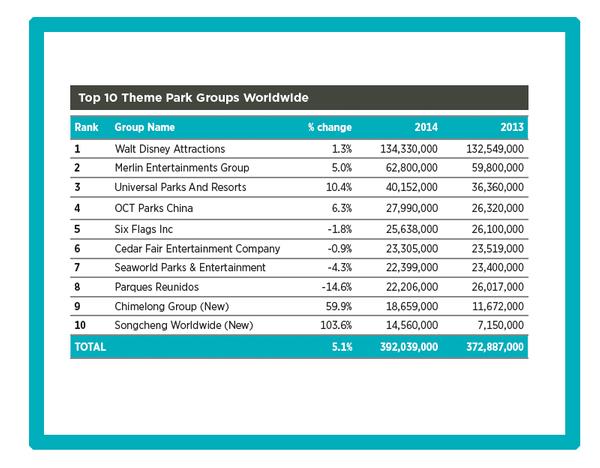

Global Overview Last year was one of global growth for the attractions industry. With aggregate attendance across the top 10 leading operator groups increasing by more than 5 per cent during 2014 to around 392 million visits, it’s clear there’s been a continuation of the sector’s post-recession recovery.

The top 25 global theme parks list has reshuffled over the past five years, with the larger Asian parks moving up. Having said that, the list is comparable with the list of five years ago, with only three of the 2009 parks dropping out and being replaced. The list of the top 25 parks in 2009 accounted for a total of 185,568,000 visitors whereas the top 25 this year accounts for a total of 223,450,000, an overall increase of an impressive 20 per cent, or the equivalent of 3.8 per cent growth every year – evidence of a global growing industry.

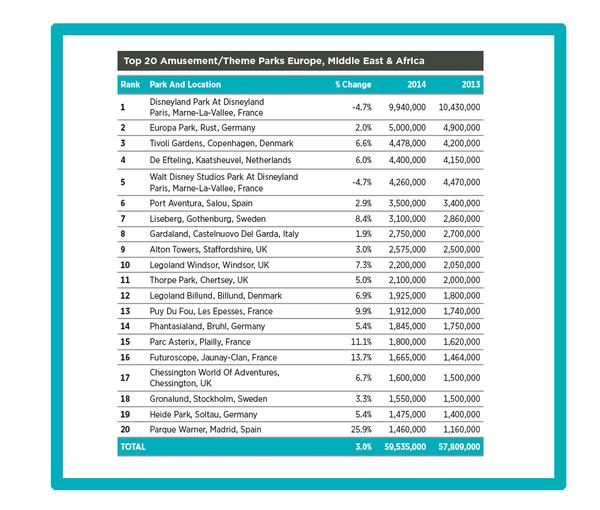

EMEA The European theme park market witnessed a return to growth in 2014, with attendance levels rebounding 3 per cent following a recession-driven lull. While in 2013 we observed a clear north-south divide in terms of attendance performance, this year no such divergence was apparent. In fact, attendance hikes were seen at all parks aside from those operated by Disney.

Operators cite the improved economic climate, better weather conditions and reinvestment in attractions as the three main reasons underpinning attendance increases. An impressive 13.7 per cent increase in attendance at Futuroscope in France has been attributed to an award-winning new ride, Raving Rabbids: The Time Machine, which is a testament to the importance of renewed investment.

With governmental backing and private sector support highly visible in the Middle East, and a young, increasingly affluent local population supplemented with an increasing tourist base, we anticipate this region to feature more heavily in the Index over the next few years as hotly anticipated mega-projects enter the market.

While five years ago European operators claimed four of the top 10 operators spots, as of 2014 only Merlin Entertainments and Parques Reunidos remain. Europe represents a mature and relatively stable marketplace; therefore, growth prospects are likely to be stronger in Asia and the Middle East than in Europe, with both upcoming regions benefitting from booming populations and rising disposable incomes.

When we compare the aggregate attendance at EMEA’s 10 most visited theme parks in 2009 to the recent figures released for EMEA in 2014, we see overall attendance has increased by just 2.5 per cent from 41.2 million to 42.2 million. This is a clear illustration of the impact of the financial downturn in Europe.

The majority of the top 10 EMEA theme parks in 2014 remain the same as five years ago, with only one new entry to the chart: Legoland Windsor, the winning concept that’s rolling out worldwide.

Operator News The top 10 operator groups have reshuffled over the past five years, reflecting a shift in energy to the East. Asian operators, such as OCT Parks China and Chimelong Group, are now snapping at the heels of industry giants, Disney, Merlin and Universal. Disney still sits head and shoulders above the rest, boasting more than double the attendance achieved by second-place Merlin, and a stronghold on the top 10 global theme parks chart, with nine parks featured.

Merlin continued its upwards trajectory throughout the course of the year, buoyed by its strongly performing Legoland parks, to achieve an aggregate attendance level of 62.8 million and maintain its position as the world’s second-largest theme park group.

This position may change, however, when the 2015 numbers come in as a result of the accident on Merlin’s Smiler ride at the Alton Towers, UK, theme park in June, which hit attendances and inflicted a £50m ($77m, ¤71m) hit on profits.

Other leading European operators Parques Reunidos and Compagnies des Alpes took the opportunity to streamline their portfolios in light of the improving economic climate, with the former having disposed of 14 FECs and one waterpark, and the latter Walibi Sud-Ouest and Dolfinarium. These groups are focusing on their core assets and anticipate rolling out new leisure parks in emerging destinations benefitting from a growing middle class.

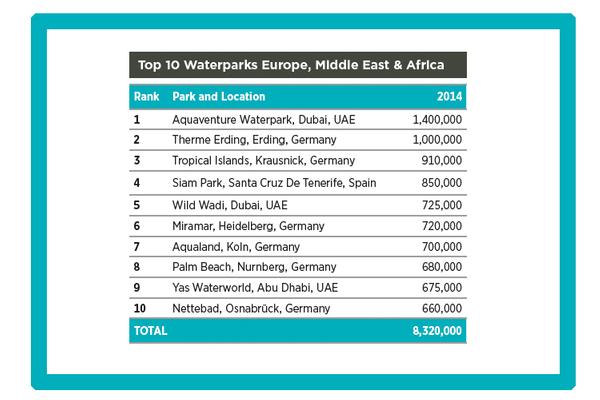

EMEA Waterparks The 2014 Theme Index includes EMEA waterparks for the first time, a sector expected to see strong growth in coming years. We anticipate uncovering more waterparks performing well in the European market as a result of this years’ publication.

Indoor facilities capture a significant market share in Northern Europe, which is not surprising given uncertainties surrounding weather. Germany reigns supreme, dominating the top 10 chart with six parks and claiming the home of Europe’s biggest waterslide, located at Therme Erding near Munich.

Germany has a long history of creating water-based attractions traditionally focused on the healing qualities of water. Over time these have increasingly turned to incorporate active play and fun waterparks. The parks listed in the EMEA top 10 waterparks are all fun parks that have a minimum of three water slides or flumes, a wave pool, retail and F&B areas, and at least two other fun elements such as tube rides, lazy river or a kids’ water play area.

The UAE features three times on the EMEA top 10 waterparks list, with Aquaventure, visited by 1.4 million people in 2014, named as the most visited waterpark in EMEA. The latest of these parks is Yas Waterworld, an example of a successful, highly themed and culturally relevant attraction, whose home-grown IP has been well-received by the local market. In contrast to many European waterparks, those in the Middle East tend to be outdoor parks with year-round operations, which has clear positive implications on attendance.

A number of waterparks operate with associated lodging, for example Splash Landings at Alton Towers, UK, and Aquaventure in Dubai. On-site accommodation can prolong length of stay (particularly for clustered attractions), allow for land use synergies (ticketing packages, increased footfall sitewide) and broaden the appeal of the destination. Lodging packages can have a detrimental impact on admission yields for individual attractions, nevertheless, the composite benefit for the destination as a whole is important and is generally overwhelmingly positive.

To IP or not to IP The role IPs play in success is hotly debated and an important question for new parks or significant extensions to existing parks.

The European market, for the most part, has grown organically over time. Although group operators feature to a greater extent these days, parks across Europe remain culturally relevant to the markets in which they operate. As a result, there are strong examples of home-grown IPs. Indeed, three of the top five European parks – Europa Park, Tivoli and De Efteling – have succeeded without international branding, creating their own storylines and IP rights.

Conversely, theme parks planned for the Middle East are large developments with a combination of resort uses. These are not only aimed at the domestic market: the expectation is that they’ll attract large swathes of tourists. Many planned parks are teaming up with globally recognised IPs that have proven records. This minimises risk and projects a clear message to the market. So, to IP or not to IP remains a question that can only be answered by looking at the target market of the planned attraction.

Read more from this issue of Spa Business magazine

Interview: Michiel Buchel

Michiel Buchel is Ecsite’s new president and CEO of the Netherland’s biggest science centre, NEMO. He shares his optimism about the science centre sector and the secrets of NEMO’s success

Attractions: All Work, All Play

KidZania, star of the edutainment world, has opened its newest franchise in London, its 17th location to date. We meet the global top team to find out what makes these small cities a big success

Analysis: Be Our Guest

TEA/AECOM’s 2014 Theme Index shows attendance growth across all regions. AECOM experts analyse the recent trends

In the fast-paced world of fitness and wellness, where high-intensity workouts push us to

our limits and the sweat pours, the importance of efficient recovery cannot be overstated. [more...]

+ More featured suppliers

COMPANY PROFILES

Pearl Tree

Pearl Tree was established in 2014 by Soraya and

Sarry Jouzy with a mission to champion

personal w [more...]

Blu Spas, Inc.

Blu is a full-service firm offering project feasibility, planning and design as well as operational [more...]

The TEA/AECOM 2014 Theme and Museum Index

indicates healthy attendance growth across all

regions, powered by the economic climate,

good weather and investment in new attractions

Aquaventure in Dubai atttracted 1.4 million visitors in 2014

The TEA/AECOM Theme and Museum Index is a collaboration of the Themed Entertainment Association (TEA) and the economics practice at AECOM, a global provider of technical-professional and management-support services.

The annual calendar-year study of global attractions attendance is a free resource for park operators, land developers and the travel industry. Top worldwide theme parks, amusement parks, waterparks, museums and theme park group operators are named and ranked by attendance, and industry trends are identified. The global market is studied as a whole, and each main region is also studied separately: the Americas, Europe and Asia. There’s also a table of the top waterparks in the world and in the US, and of the top global chain operators.

Here, AECOM looks at the numbers and makes comparisons with the 2009 listings.

Global Overview Last year was one of global growth for the attractions industry. With aggregate attendance across the top 10 leading operator groups increasing by more than 5 per cent during 2014 to around 392 million visits, it’s clear there’s been a continuation of the sector’s post-recession recovery.

The top 25 global theme parks list has reshuffled over the past five years, with the larger Asian parks moving up. Having said that, the list is comparable with the list of five years ago, with only three of the 2009 parks dropping out and being replaced. The list of the top 25 parks in 2009 accounted for a total of 185,568,000 visitors whereas the top 25 this year accounts for a total of 223,450,000, an overall increase of an impressive 20 per cent, or the equivalent of 3.8 per cent growth every year – evidence of a global growing industry.

EMEA The European theme park market witnessed a return to growth in 2014, with attendance levels rebounding 3 per cent following a recession-driven lull. While in 2013 we observed a clear north-south divide in terms of attendance performance, this year no such divergence was apparent. In fact, attendance hikes were seen at all parks aside from those operated by Disney.

Operators cite the improved economic climate, better weather conditions and reinvestment in attractions as the three main reasons underpinning attendance increases. An impressive 13.7 per cent increase in attendance at Futuroscope in France has been attributed to an award-winning new ride, Raving Rabbids: The Time Machine, which is a testament to the importance of renewed investment.

With governmental backing and private sector support highly visible in the Middle East, and a young, increasingly affluent local population supplemented with an increasing tourist base, we anticipate this region to feature more heavily in the Index over the next few years as hotly anticipated mega-projects enter the market.

While five years ago European operators claimed four of the top 10 operators spots, as of 2014 only Merlin Entertainments and Parques Reunidos remain. Europe represents a mature and relatively stable marketplace; therefore, growth prospects are likely to be stronger in Asia and the Middle East than in Europe, with both upcoming regions benefitting from booming populations and rising disposable incomes.

When we compare the aggregate attendance at EMEA’s 10 most visited theme parks in 2009 to the recent figures released for EMEA in 2014, we see overall attendance has increased by just 2.5 per cent from 41.2 million to 42.2 million. This is a clear illustration of the impact of the financial downturn in Europe.

The majority of the top 10 EMEA theme parks in 2014 remain the same as five years ago, with only one new entry to the chart: Legoland Windsor, the winning concept that’s rolling out worldwide.

Operator News The top 10 operator groups have reshuffled over the past five years, reflecting a shift in energy to the East. Asian operators, such as OCT Parks China and Chimelong Group, are now snapping at the heels of industry giants, Disney, Merlin and Universal. Disney still sits head and shoulders above the rest, boasting more than double the attendance achieved by second-place Merlin, and a stronghold on the top 10 global theme parks chart, with nine parks featured.

Merlin continued its upwards trajectory throughout the course of the year, buoyed by its strongly performing Legoland parks, to achieve an aggregate attendance level of 62.8 million and maintain its position as the world’s second-largest theme park group.

This position may change, however, when the 2015 numbers come in as a result of the accident on Merlin’s Smiler ride at the Alton Towers, UK, theme park in June, which hit attendances and inflicted a £50m ($77m, ¤71m) hit on profits.

Other leading European operators Parques Reunidos and Compagnies des Alpes took the opportunity to streamline their portfolios in light of the improving economic climate, with the former having disposed of 14 FECs and one waterpark, and the latter Walibi Sud-Ouest and Dolfinarium. These groups are focusing on their core assets and anticipate rolling out new leisure parks in emerging destinations benefitting from a growing middle class.

EMEA Waterparks The 2014 Theme Index includes EMEA waterparks for the first time, a sector expected to see strong growth in coming years. We anticipate uncovering more waterparks performing well in the European market as a result of this years’ publication.

Indoor facilities capture a significant market share in Northern Europe, which is not surprising given uncertainties surrounding weather. Germany reigns supreme, dominating the top 10 chart with six parks and claiming the home of Europe’s biggest waterslide, located at Therme Erding near Munich.

Germany has a long history of creating water-based attractions traditionally focused on the healing qualities of water. Over time these have increasingly turned to incorporate active play and fun waterparks. The parks listed in the EMEA top 10 waterparks are all fun parks that have a minimum of three water slides or flumes, a wave pool, retail and F&B areas, and at least two other fun elements such as tube rides, lazy river or a kids’ water play area.

The UAE features three times on the EMEA top 10 waterparks list, with Aquaventure, visited by 1.4 million people in 2014, named as the most visited waterpark in EMEA. The latest of these parks is Yas Waterworld, an example of a successful, highly themed and culturally relevant attraction, whose home-grown IP has been well-received by the local market. In contrast to many European waterparks, those in the Middle East tend to be outdoor parks with year-round operations, which has clear positive implications on attendance.

A number of waterparks operate with associated lodging, for example Splash Landings at Alton Towers, UK, and Aquaventure in Dubai. On-site accommodation can prolong length of stay (particularly for clustered attractions), allow for land use synergies (ticketing packages, increased footfall sitewide) and broaden the appeal of the destination. Lodging packages can have a detrimental impact on admission yields for individual attractions, nevertheless, the composite benefit for the destination as a whole is important and is generally overwhelmingly positive.

To IP or not to IP The role IPs play in success is hotly debated and an important question for new parks or significant extensions to existing parks.

The European market, for the most part, has grown organically over time. Although group operators feature to a greater extent these days, parks across Europe remain culturally relevant to the markets in which they operate. As a result, there are strong examples of home-grown IPs. Indeed, three of the top five European parks – Europa Park, Tivoli and De Efteling – have succeeded without international branding, creating their own storylines and IP rights.

Conversely, theme parks planned for the Middle East are large developments with a combination of resort uses. These are not only aimed at the domestic market: the expectation is that they’ll attract large swathes of tourists. Many planned parks are teaming up with globally recognised IPs that have proven records. This minimises risk and projects a clear message to the market. So, to IP or not to IP remains a question that can only be answered by looking at the target market of the planned attraction.

Read more from this issue of Spa Business magazine

Interview: Michiel Buchel

Michiel Buchel is Ecsite’s new president and CEO of the Netherland’s biggest science centre, NEMO. He shares his optimism about the science centre sector and the secrets of NEMO’s success

Attractions: All Work, All Play

KidZania, star of the edutainment world, has opened its newest franchise in London, its 17th location to date. We meet the global top team to find out what makes these small cities a big success

Analysis: Be Our Guest

TEA/AECOM’s 2014 Theme Index shows attendance growth across all regions. AECOM experts analyse the recent trends

Mass protests have been taking place since Monday 1 June in Albania over the development of

a luxury resort by Donald Trump’s daughter Ivanka Trump and her husband Jared Kushner.

Global Wellness Day (GWD) marked its 15th anniversary on Saturday 13 June 2026, with the

theme: #JoyMagenta – a celebration of the healing qualities of simple gestures and activities

that spark joy.

Global luxury hospitality brand, Six Senses, has partnered with longevity healthcare provider,

HUM2N, to launch a clinic at Six Senses London, at The Whiteley.

As part of its first hotel partnership, Mayrlife – the medical health resort company known for its

site in Altaussee, Austria – has launched a day clinic at the Rosewood Vienna.

Premium London health club, KX Chelsea, will imminently unveil its most significant

redevelopment since its launch in 2002 to create an integrated wellness model combining

training, recovery and relaxation.

Rosewood Le Guanahani St Barth, on the northeast coast of Saint Barthélemy in the French

West Indies, is offering a programme of ocean-inspired yoga classes between 8-14 June to

celebrate Global Wellness Day (GWD).

Hotel de France, located on the British Isle of Jersey, has created a wellness retreat package

that includes a hot yoga session that will take place in Jersey Zoo’s butterfly sanctuary.

The Ritz-Carlton, Langkawi, in Malaysia, has revealed a schedule for Global Wellness Day

(GWD) that includes guided rainforest walks, mindful movement and guided coastal meditation

experiences.

Longevitix, a clinical platform for preventive and longevity medicine, has launched its AI-

powered intelligence system to help physicians deliver continuous, personalised longevity-

focused care at scale.

Atmantan Wellness Centre, an integrative wellness destination in Mulshi, near Pune in India, is

expanding its portfolio by adding a new centre in Hyderabad that will launch between 2028 and

2029.

In the fast-paced world of fitness and wellness, where high-intensity workouts push us to

our limits and the sweat pours, the importance of efficient recovery cannot be overstated. [more...]

+ More featured suppliers

COMPANY PROFILES

Pearl Tree Pearl Tree was established in 2014 by Soraya and

Sarry Jouzy with a mission to champion

personal w [more...]